Making a difference through charitable giving feels great. Getting a tax break for your generosity? Even better.

Tax deductions for charitable donations can significantly reduce your tax bill, but only if you navigate the rules correctly. The IRS has specific requirements about which organizations qualify, how much you can deduct, and what documentation you need to keep. Miss a step, and you might lose out on valuable deductions or face questions during an audit.

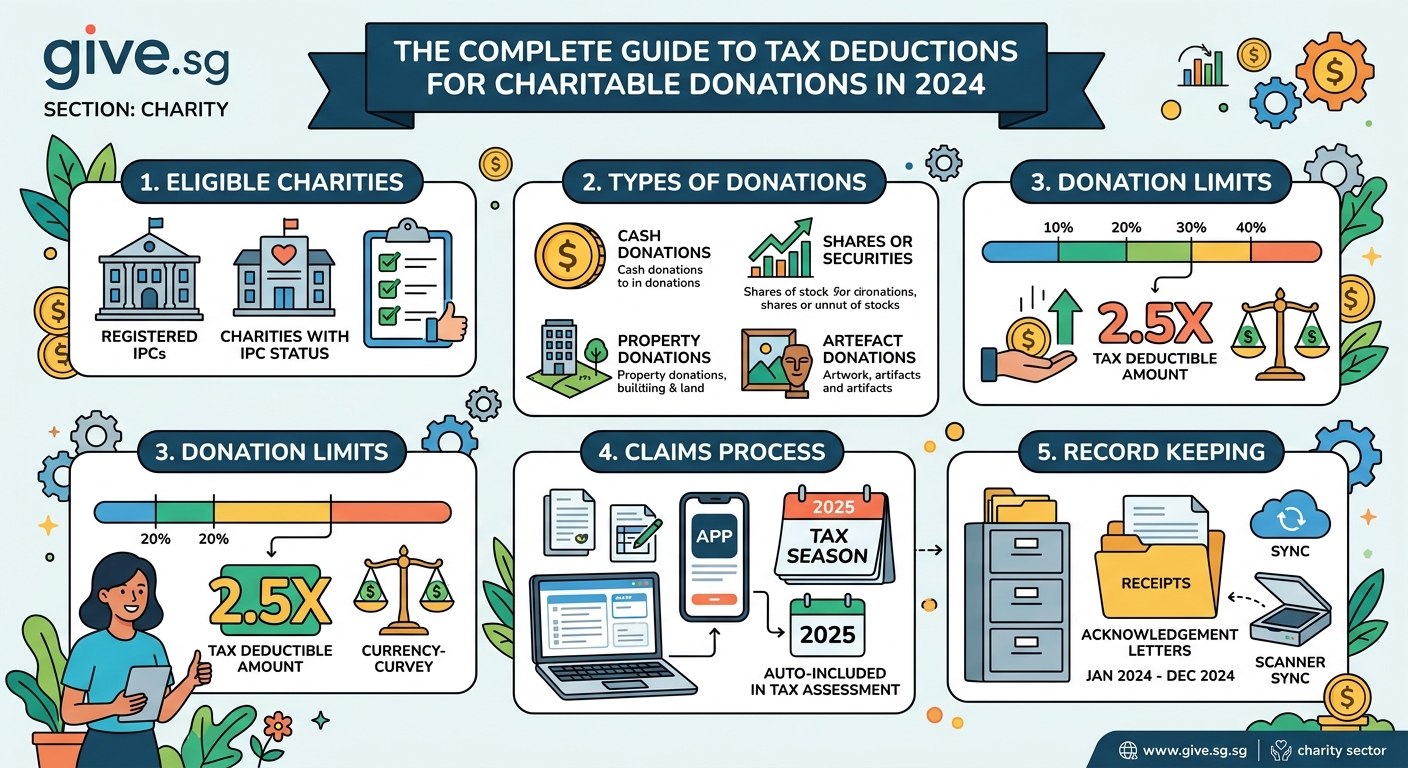

Tax deductions for charitable donations let you reduce taxable income when you give to qualified organizations. You must itemize deductions, donate to IRS-approved nonprofits, and maintain proper documentation. Deduction limits typically range from 30% to 60% of your [adjusted gross income](https://www.irs.gov/e-file-providers/definition-of-adjusted-gross-income) depending on the gift type. Cash donations require bank records or receipts, while non-cash gifts over $250 need written acknowledgments and appraisals for high-value items.

Understanding charitable contribution deduction basics

Not every donation qualifies for a tax break. The IRS only allows deductions for contributions to qualified organizations, which include most nonprofits with 501(c)(3) status.

Churches, temples, mosques, and other religious organizations qualify automatically. So do most educational institutions, hospitals, and publicly supported charities. Political campaigns, candidates, and lobbying groups do not qualify, no matter how much you support their cause.

You also need to itemize deductions on Schedule A of your tax return. The standard deduction for 2024 is $14,600 for single filers and $29,200 for married couples filing jointly. If your total itemized deductions (including charitable gifts, mortgage interest, and state taxes) don’t exceed these amounts, you won’t benefit from claiming charitable contributions.

Your adjusted gross income (AGI) determines how much you can deduct in a single year. Most cash donations are limited to 60% of your AGI. Donations of appreciated assets like stocks or real estate typically max out at 30% of AGI. Any excess can roll forward for up to five years.

Documentation requirements you cannot ignore

The IRS takes documentation seriously. Lose your records, lose your deduction.

For cash donations under $250, you need a bank record or receipt from the charity. A canceled check works. So does a credit card statement showing the transaction. A text message confirmation from a mobile giving platform counts too.

Once you hit $250 or more for a single contribution, you need a written acknowledgment from the organization. This must include the donation amount, whether you received anything in return, and an estimate of any goods or services provided. The charity should send this automatically, but if they don’t, ask before you file your taxes.

Non-cash donations follow stricter rules. Items worth less than $250 need a receipt from the charity. Between $250 and $500, you need that written acknowledgment plus your own records describing what you donated and its condition.

Donations between $500 and $5,000 require Form 8283, Section A. You’ll need to describe the property, how you acquired it, and your cost basis.

Above $5,000, you enter serious territory. You need a qualified appraisal from an independent appraiser, completed no earlier than 60 days before the donation and filed with your return using Form 8283, Section B. Cars, boats, and planes have their own special rules requiring Form 1098-C from the charity.

Maximizing deductions with strategic giving

Smart donors think beyond writing checks. Different types of contributions offer different tax advantages.

Donating appreciated stocks or mutual funds you’ve held for more than a year lets you deduct the full fair market value while avoiding capital gains tax on the appreciation. If you bought shares for $5,000 that are now worth $15,000, you can deduct $15,000 and never pay tax on that $10,000 gain.

Qualified charitable distributions (QCDs) from IRAs work well for donors over 70½. You can transfer up to $105,000 directly from your IRA to a qualified charity in 2024. The distribution doesn’t count as taxable income and satisfies your required minimum distribution if you’re over 73.

Bunching donations into alternating years helps when you’re close to the standard deduction threshold. Instead of giving $10,000 annually, donate $20,000 every other year. You itemize in high-donation years and take the standard deduction in low-donation years, maximizing your total tax benefit.

Donor-advised funds let you take an immediate deduction for a large contribution, then distribute grants to charities over time. You might contribute $50,000 in a high-income year, claim the full deduction, then recommend grants of $10,000 annually to your favorite causes.

Common mistakes that trigger IRS scrutiny

Even well-intentioned donors make errors that cost them deductions or invite audits.

Overvaluing donated items ranks as the most common problem. That couch you paid $2,000 for ten years ago isn’t worth $2,000 today. The IRS expects you to use thrift store pricing for used clothing, furniture, and household goods. Most items in good condition fetch 20% to 40% of original retail value.

Claiming deductions without proper substantiation creates problems during audits. The IRS can disallow your entire charitable deduction if you can’t produce required documentation, even if you genuinely made the donations.

Deducting the value of your time or services doesn’t work. You can deduct mileage driven for charity work at 14 cents per mile in 2024, and you can deduct supplies you purchase, but your hourly rate as a volunteer generates no deduction.

Failing to reduce your deduction when you receive benefits trips up many donors. If you pay $500 for a charity dinner ticket and the meal is worth $100, you can only deduct $400. The charity should tell you the deductible portion, but you’re responsible for getting it right.

Here’s a breakdown of common documentation errors and how to fix them:

| Mistake | Why It Fails | Correct Approach |

|---|---|---|

| No receipt for cash under $250 | IRS requires bank record or written communication | Keep bank statements, canceled checks, or email confirmations |

| Missing written acknowledgment over $250 | Required by law regardless of other documentation | Request acknowledgment letter from charity before filing |

| Self-appraising items over $5,000 | IRS requires independent qualified appraisal | Hire certified appraiser and file Form 8283, Section B |

| Deducting full ticket price for events | Must subtract fair market value of benefits received | Use deductible amount shown on ticket or receipt |

| Using original purchase price for used items | Must use fair market value at time of donation | Research thrift store prices for similar items |

Special considerations for high-value donations

Large charitable contributions require extra planning and documentation.

Real estate donations can generate substantial deductions but involve complex rules. You need an appraisal, environmental assessment, and clear title. If the property has appreciated significantly, you might face alternative minimum tax issues. Conservation easements offer special benefits but attract intense IRS scrutiny after years of abusive tax shelters.

Art, jewelry, and collectibles valued over $20,000 need appraisals from experts recognized by the IRS Art Advisory Panel. The charity must use the item for a purpose related to its mission, or your deduction drops to your cost basis rather than fair market value. If you donate a painting to a hospital that immediately sells it, you can only deduct what you originally paid.

Closely held business interests and intellectual property follow specialized rules. You typically deduct fair market value, but the IRS will examine the valuation closely. Some intellectual property donations require you to report additional income if the charity later generates revenue from the asset.

“The biggest mistake I see is donors making large contributions without consulting a tax professional first. A $50,000 donation might seem straightforward, but the tax implications vary dramatically based on what you give, when you give it, and your overall financial situation. Spending a few hundred dollars on professional advice can save thousands in taxes or prevent costly errors.” – Tax attorney with 20 years of nonprofit experience

Year-end planning strategies

December 31 creates a hard deadline for current-year deductions. Contributions must be completed by that date to count.

Credit card donations count when charged, not when you pay the bill. A donation charged on December 31 counts for 2024 even if you pay the credit card bill in January 2025.

Checks count when mailed, not when cashed. Mail your check by December 31, and it qualifies for the current year even if the charity deposits it weeks later. Keep proof of mailing date.

Online donations must process by midnight on December 31 in your time zone. Don’t wait until the last minute, as website crashes or payment processing delays could push your contribution into the next year.

Stock transfers take longer. Start the process at least a week before year-end to ensure the shares transfer to the charity’s account before December 31. The transfer date, not the date you initiate the gift, determines which tax year applies.

Follow these steps to ensure your year-end donations qualify:

- Verify the organization’s tax-exempt status using the IRS Tax Exempt Organization Search tool before donating.

- Make your contribution by December 31 using a method with clear documentation (check, credit card, or bank transfer).

- Request written acknowledgment immediately for any single donation of $250 or more.

- Photograph and inventory any non-cash donations before delivery, noting condition and fair market value.

- Save all documentation in a dedicated tax file, including receipts, acknowledgment letters, appraisals, and bank records.

- Calculate whether itemizing deductions exceeds your standard deduction before filing.

Recordkeeping best practices

Good records protect your deductions and simplify tax preparation.

Create a dedicated folder (physical or digital) for charitable donation records each tax year. Store receipts, acknowledgment letters, appraisals, and bank statements together.

Take photos of donated items before delivery. Visual documentation helps if the IRS questions your valuation. A photo of your donated furniture in good condition supports your claimed value better than memory alone.

Track mileage for volunteer work throughout the year. Waiting until tax time to estimate miles driven for charity work leads to errors and weak documentation. A simple mileage log with dates, destinations, and miles driven satisfies IRS requirements.

Keep records for at least three years after filing, but seven years is safer. The IRS can audit returns up to three years back in most cases, six years if they suspect substantial underreporting.

Consider these items worth keeping for charitable donation records:

- Bank statements showing electronic transfers

- Canceled checks with donation notations

- Credit card statements highlighting charitable charges

- Email confirmations from online donation platforms

- Written acknowledgment letters for donations over $250

- Form 1098-C for vehicle donations

- Form 8283 with appraisals for high-value non-cash gifts

- Photos and condition descriptions for donated property

- Mileage logs for volunteer driving

Making your charitable giving count

Tax benefits shouldn’t drive your charitable decisions, but they make generosity more affordable.

Understanding the rules helps you give more effectively. When you know how to maximize deductions, you can stretch your charitable budget further or give the same amount at lower after-tax cost.

The key is planning ahead. Last-minute donations on December 31 often mean missed opportunities for better tax strategies. Review your charitable giving in October or November each year. Calculate whether you’re close to the itemization threshold. Consider bunching donations or using appreciated assets instead of cash.

Work with qualified professionals for large or complex donations. Tax laws change regularly, and mistakes can be expensive. A good tax advisor pays for themselves many times over when you’re making substantial charitable contributions.

Start building better donation habits today. Set up a simple recordkeeping system. Research the tax-exempt status of organizations you support. Track your contributions throughout the year rather than scrambling at tax time. Your future self will thank you when tax season arrives, and the causes you care about will benefit from your informed, strategic generosity.